As we step into September, all eyes are on the Federal Reserve. The consensus is clear: most experts anticipate that the Fed will cut the Federal Funds Rate at their upcoming meeting. This expectation is driven by signs of cooling inflation and a slowing job market. Mark Zandi, Chief Economist at Moody’s Analytics, commented:

“They’re prepared to cut, as long as there’s no unexpected spike in inflation between now and September, which is unlikely.”

But what does this potential rate cut mean for the housing market and, more importantly, for you as a buyer or seller?

Why the Federal Funds Rate Cut Matters

The Federal Funds Rate plays a significant role in influencing mortgage rates, alongside other factors like the economy and global events.

When the Fed lowers this rate, it reflects broader economic conditions, and mortgage rates often adjust in response. While a single rate cut may not result in a sharp drop in mortgage rates, it can contribute to the gradual decrease that’s already in motion.

Mike Fratantoni, Chief Economist at the Mortgage Bankers Association (MBA), notes:

“Once the Fed begins a rate-cutting cycle, we expect mortgage rates to trend slightly lower.”

Moreover, this expected rate cut likely marks the start of a series. Lawrence Yun, Chief Economist at the National Association of Realtors (NAR), adds:

“Typically, the rate-cutting cycle involves multiple reductions. We’re likely to see six to eight rounds of cuts continuing into 2025.”

The Expected Impact on Mortgage Rates

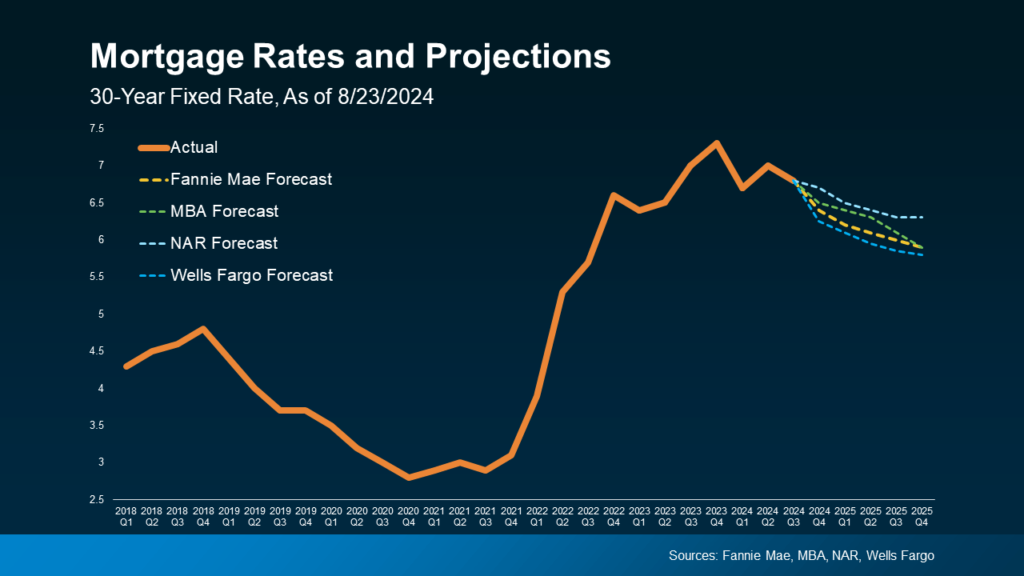

Industry experts predict that mortgage rates will gradually decline through 2025, partly due to the Fed’s anticipated rate cuts. Here’s what some of the leading forecasts from Fannie Mae, MBA, NAR, and Wells Fargo suggest for mortgage rates over the next few years.

(Sample graph would be included here)

This ongoing shift in rates could create favorable conditions for both homebuyers and sellers, making it essential to stay informed as the Fed’s decisions unfold.

With recent improvements in inflation and signs of a cooling job market, a cut in the Federal Funds Rate is expected to lead to a moderate decline in mortgage rates (illustrated by the dotted lines). Here are two key reasons why this is great news for both buyers and sellers:

1. Easing the Lock-In Effect

Lower mortgage rates could help alleviate the “lock-in effect” for current homeowners. This is when people feel stuck in their current homes because today’s higher rates make it unattractive to give up the lower rate they locked in when they originally purchased.

If concerns about losing your low-rate mortgage have held you back from selling, a slight reduction in rates could make moving more appealing. However, this likely won’t lead to a surge of new sellers, as many will still be cautious about trading their current low rates for higher ones.

2. Encouraging More Buyer Activity

For prospective buyers, any drop in mortgage rates can make homeownership more affordable. A reduction in rates could lower monthly payments, potentially making it easier for you to enter the market if you’ve been waiting for the right opportunity.

What Should You Do?

While the anticipated rate cut probably won’t cause a sharp drop in mortgage rates, it will likely continue the gradual decline already in progress.

This positive shift is a good sign for the future of the housing market, but it’s also important to focus on your personal circumstances. As Jacob Channel, Senior Economist at LendingTree, wisely points out:

“Trying to time the market perfectly is nearly impossible. If you’re waiting for ideal conditions, you might wait forever. Buy now if it makes sense for your situation.”

Bottom Line

With inflation easing and job growth slowing, the expected Federal Funds Rate cut should gradually help lower mortgage rates, creating potential opportunities for both buyers and sellers. If you’re considering a move, let’s connect so you can be ready when the time is right for you.